I’ve been seriously thinking about upgrading to a 2024 Mustang GT. There’s actually one for sale not too far from me, and I’m pretty close to having enough saved up, about $5,000. The thing is, I’m torn about whether it’s worth pulling the trigger on this new model.

For a bit of context, I’m currently driving a 2015 EcoBoost Premium, and it’s been a great ride. My girlfriend even mentioned that she’s interested in taking over my car if I go ahead with the new Mustang. She’s always loved Mustangs too, so it could be a fun way for us both to enjoy these iconic cars.

I’m just trying to weigh whether the 2024 model really offers enough improvements and new features to justify the expense and the change from my current car. Has anyone here had a chance to drive the 2024 GT and can share how it stacks up against the earlier models?

People should avoid taking on unfavorable car loans.

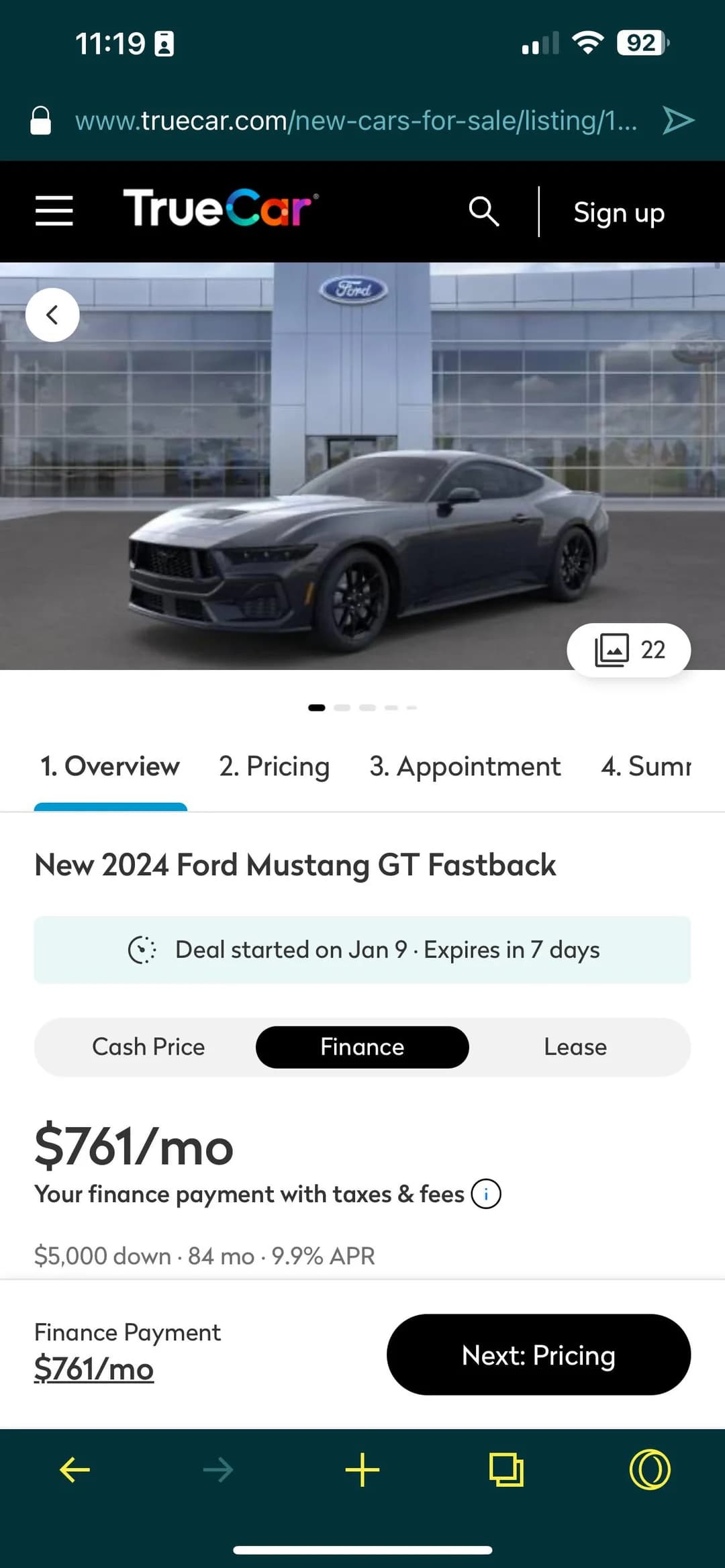

An 84-month term is a definite red flag, and a 9.9% interest rate is also a big no-no. Combine both, and it’s even worse.

It’s perfectly fine not to have everything right away. By managing your finances and being patient, you’ll eventually have the chance to enjoy the things you want.

I only talk about what I’ve experienced personally. I’ve been in the position where I was so eager for a new car that I’d have done anything to get it. Now that I’m older, I look back and just shake my head. Buying a GT just for the sake of the market isn’t worth it. They don’t retain their value well and are overpriced when new. If you end up getting bored with it and start looking for something else in a year or two, you could end up losing a lot of money.

A 72-month loan term is really stretching it. You’ll spend around 36 months just breaking even on the car.

Personally, I make payments every two weeks instead of monthly. I also round up my payments to pay a little extra and fit in an additional payment each year. For example, with a $425 monthly payment, I pay $213 every two weeks. That’s 26 $213 payments versus 12 $425 monthly payments.

I round that $213 up to $300, which usually lets me pay off the vehicle 18-24 months earlier than planned or build up extra equity. The quicker you can reduce your loan balance, the better.

Wow, I hadn’t thought about making payments every two weeks instead of monthly. What are the actual benefits of doing that? Does it help reduce the interest you pay over time?

Actually, you are paying off the loan early by making biweekly payments. Even if you only make 26 half-payments a year, that’s equivalent to an extra full payment annually (26 x 0.5 = 13 payments compared to the usual 12). Over about 5 years, this can help you pay off your car 5 months earlier.

I personally pay off my car sooner by increasing my biweekly payments. Most reputable institutions don’t mind if you make extra payments.